Ever imagined what would happen if your cherished jewelry vanished or suffered severe damage? For many, it’s more than just the loss of a mere object. It’s the loss of memories, moments, and sentiments.

If you’re thinking of investing in a safety net for your treasured pieces, jewelry insurance might be the answer. In this guide, we get into the heart of jewelry insurance claims. We cover how they work and how you can get the most out of them.

You probably have insurance for your home, your car, and perhaps your medical needs. And why not? After all, it pays to protect yourself and your things. So shouldn’t that apply to your jewelry, too?

Unfortunately, jewelry insurance often becomes important only after something’s happened to our cherished pieces. The good news? It doesn’t have to be this way!

Let’s say you’re interested in insuring jewelry from your collection. Smart move. But have you ever stopped to think, “How do jewelry insurance claims work?”

It’s a fair question to ask, mainly because jewelry insurance is a bit different from traditional insurance policies. So let’s take a look, shall we?

Like these other insurance policies, jewelry insurance is all about peace of mind. It ensures that if your favorite piece of jewelry gets damaged or stolen, you aren’t left grappling with both an emotional loss and a financial one.

Here’s a quick breakdown:

Imagine you’ve saved up and bought a piece of jewelry that not only costs a lot but also holds sentimental value. Now, imagine losing it or finding it damaged. The emotional pain is inevitable, but the financial strain? That can be avoided thanks to jewelry insurance.

Think about it this way. Let’s say you’re already investing in making your living space perfect with Homebody. Protecting your valuable jewelry should be the next logical step in ensuring everything you cherish is safe.

After all, the peace of mind knowing that your jewelry insurance coverage is comprehensive can be priceless.

Is jewelry insurance worth it? The answer largely depends on the emotional and financial value of your jewelry collection. But when you consider the relatively low jewelry insurance cost compared to the potential replacement value, it’s a smart investment.

Still not sure? We'll explore the ins and outs of the jewelry insurance claim process. Whether you’re insuring an engagement ring, a family heirloom, or a newly purchased piece, this is the vital info you need to know.

A lot of us assume that when a precious piece of jewelry goes missing or gets damaged, our homeowners or renters insurance will step up. But how exactly does homeowners insurance cover jewelry, and what are its limitations?

At its core, most homeowners and renters insurance policies do offer some type of jewelry coverage, typically under the personal property umbrella. It works like this:

Do the limitations of standard insurance policies make you uneasy? Thankfully, there are more tailored routes to ensure your jewelry is aptly protected:

The options above offer great ways to leverage your homeowners or renters insurance. But maybe you’re on the lookout for something more customized. Jewelry insurance companies can offer policies specifically designed for precious stones and metals.

When filing a claim, you want to know that your policy has not just your jewelry covered but also your needs. So let’s see what options you have.

For those who won’t settle for anything less than comprehensive protection for their precious trinkets, specialized insurance is the answer. Here’s what sets specialized jewelry insurance apart.

While typical homeowners insurance might have limitations, specialized jewelry insurance companies step up their game. Their policies don’t just stop at theft or damage; they also include preventive maintenance to ensure the longevity of your jewelry.

When a jewelry insurance policy boasts of “all risks” coverage, it’s essentially promising comprehensive protection. These policies are crafted to insure jewelry against a gamut of risks, only excluding a few specific ones.

However, always read the fine print. While the “all risks” tag sounds promising, there might be specific exclusions like intentional damage, regular wear and tear, or certain natural disasters.

One of the best features of high-ranking jewelry insurance policies is their commitment to restoring your prized possession to its original glory. In the unfortunate event of damage, they don’t just compensate you.

Many of these insurance companies have connections with reputed jewelers. Should you need to file a claim, they ensure your jewelry is repaired or replaced by a trusted jeweler.

Choosing the right jewelry insurance company is crucial. Trusted names like Jewelers Mutual offer policies tailored specifically for jewelry enthusiasts.

From getting your jewelry appraised to understanding the nuances of how replacement cost coverage works, these companies guide you every step of the way.

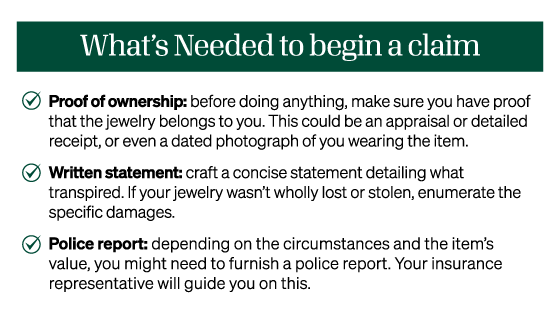

Now that you know how jewelry insurance works, it’s time to move on to the claims process. This knowledge will prepare you should you ever be in the unfortunate position of having to file a claim.

OK, so your beloved jewelry was lost, stolen, or damaged. You know you have to file a claim, but what does that entail? It can seem intimidating from a distance. But we’ve broken down the process so that you can seek restitution and get on with your life.

Ready to proceed? Here’s what’s next:

Now we need to talk about what’s covered. This will be different based on what jewelry insurance company you have. So that we have an example to look at, let’s use Jewelers Mutual:

Not everything is going to be covered, no matter how good your insurance policy is. Using Jewelers Mutual again, here’s what they don’t cover:

Understanding the ins and outs of the jewelry insurance claim process ensures you’re ready for almost anything. Remember, every piece of jewelry holds a story. With the right insurance coverage, that story can continue for generations to come.

You might think all jewelry warranties and service plans are the same. But look closer, and you’ll see that they offer different types of protection.

Think of these as a safety net for those unexpected manufacturing mistakes. Maybe a clasp malfunctions, or a setting isn’t quite right. That’s where warranties step in.

However, if your treasured necklace slips off while you’re diving into ocean waves or if it becomes a target for thieves, warranties often look the other way.

We also need to point out that keeping your warranty active often means regular inspections by the jeweler. For some consumers, this is a hassle they’d rather not deal with.

These are your go-to for life’s everyday jewelry wear and tear. Had a change in ring size? Maybe you noticed a gemstone wobbling in its setting.

Service plans are designed for such fixes. But remember, they’re not your guardian angels against theft or if you suffer a complete loss of your piece. As we’ve discussed, there are separate coverage options for things like that.

Trying to wrap your head around jewelry protection can be dizzying. But at Homebody, we’re all about clarity. So let us break down things in simple terms. Soon, you’ll be able to pick out a plan that works for you.

Your jewelry box consists of only a few cherished items. What’s more, their value doesn’t exceed the limit set in your homeowners or renters insurance. Guess what? You’re probably already well-covered! There’s probably no need to shell out money for added coverage.

Are you the proud owner of a piece that’s the talk of every party? Or perhaps, over the years, your modest collection has grown into a veritable treasure trove. In such cases, blanket or scheduled personal property coverage might be more your speed.

Are you the type who wants all-encompassing protection for your collection? The type that ensures your jewelry is covered without any unexpected hikes in your home insurance premiums? Then specialized jewelry insurance is for you.

Don’t hesitate to shop around, either. Just as your jewelry deserves the best protection, you deserve the best rates. No matter which option you ultimately decide on, you can find affordable coverage that keeps your prized possessions safe.

Your jewelry tells your story. It carries memories of milestone moments, tokens of love, and personal expressions. Taking a proactive approach to protect your baubles means ensuring your memories stay intact, no matter what.

At Homebody, we’re all about making home the best place on earth. So whether it’s an apartment you’re renting or a necklace passed down generations, give it the protection it deserves.