Determining the amount of auto insurance you need doesn’t have to be complicated. Whether you’re a first-time buyer or reevaluating your current policy, understanding “how much auto insurance do I need” is crucial. In this straight-to-the-point guide, you’ll learn how to balance state requirements with personal asset protection to tailor coverage options like liability, collision, and comprehensive insurance to your life’s needs, ensuring you’re fully protected without overpaying.

You’ve probably heard the term ‘liability coverage’ tossed around. At its core, liability insurance is your safety net. It’s there to cover property damage and injuries to others if you’re at fault in a car accident, safeguarding you if someone decides to sue you for the damage or injuries you cause while driving. Think of it as your financial shield on the road.

Determining how much car insurance you need can be tricky. Experts suggest coverage of $100,000 per person and $300,000 per accident for bodily injuries, plus a minimum of $100,000 in property damage liability. But what exactly are bodily injury liability and property damage liability? It’s time to delve into these key components.

In a nutshell, bodily injury liability covers medical bills and lost income for people hurt in an accident you’re responsible for. So, if your accident results in someone else having to hang up their work boots for a while or rack up some hefty hospital bills, this coverage has got you sorted.

Now, here’s a crucial question - how much liability insurance should you get? The recommendation is to aim for at least $500,000 worth of bodily injury liability coverage. This will help you meet or exceed the liability coverage limits required by your state and protect your assets in the event of a claim.

Moving on to the other side of the coin - property damage liability. This coverage looks after the damages to someone else’s stuff, usually their car, if you’re at fault in an accident. It’s like a safety net for your wallet when you’re responsible for someone else’s crunched fender or dented door.

Determining the ideal protection amount isn’t a one-size-fits-all approach. Various factors come into play, such as your car’s make and model, your driving experience, and even your ZIP code. A cardinal rule to remember? Make sure your coverage can withstand significant expenses if you face a lawsuit, typically exceeding the state’s minimum requirements.

Beyond liability coverage, there’s more to the car insurance story - collision and comprehensive insurance. These coverages are like your vehicle’s bodyguards, standing guard against different situations. Car insurance coverage, such as collision coverage, pays for costs from accidents with other vehicles or objects, while comprehensive coverage shields you from theft and damage from non-collision events like fire, natural disasters, and vandalism.

Even though state laws don’t mandate these coverages, they are vital if you can’t readily replace your vehicle with cash or afford the repair costs. So, when should you consider dropping them? If the insurance costs approach or exceed your car’s value, then it may be time to reconsider collision and comprehensive coverage.

Let’s zoom in on collision coverage. This superhero of insurance pays for the repair or replacement of your car if you get into an accident, no matter whose fault it is. It’s like having a safety net for your ride, giving you peace of mind knowing your car is covered for fixes or replacements after an accident.

When is collision coverage a good idea? If you aim to shield your car from damage in the event of an accident, irrespective of who caused it, collision coverage is a wise choice. While not obligatory, it’s a strategic decision if you want to cover your car repair costs, particularly as your vehicle’s value diminishes with time.

Next up, comprehensive insurance. This coverage steps up for things like:

Basically non-traffic-related incidents. It’s like having a security guard for your car, protecting it from all sorts of unexpected events.

But what doesn’t it pay for? Collision incidents. That’s right, comprehensive insurance doesn’t cover accidents with other vehicles. That’s where collision insurance steps in. So, comprehensive insurance and collision coverage work hand in hand to provide you with extensive protection for your vehicle.

Now, let’s look beyond the basic trio of liability, collision, and comprehensive coverages. There are additional coverage options that can offer you even more protection. These include uninsured motorist coverage, medical payments coverage, and personal injury protection.

These additional coverages are like an extra layer of armor, offering you more security and peace of mind. They ensure that you’re financially protected, even in situations that traditional car insurance might not cover. Determining if these additional coverages fit your needs can be challenging. Let’s explore how to make this decision.

Imagine you’re in an accident, and the other driver doesn’t have insurance. Nightmare, right? That’s where uninsured motorist coverage (UM) comes into play. It covers your medical expenses if you get into an accident with an uninsured driver or a hit-and-run incident.

But what if the other driver has insurance but not enough to cover all the damages? Enter underinsured motorist coverage (UIM). This coverage steps in when the other driver’s insurance can’t cover all the costs of the accident. It’s like having a backup parachute when the main one fails to open.

Medical Payments Coverage (MedPay) and Personal Injury Protection (PIP) are two additional coverages designed to alleviate the financial burden of medical bills after an accident. MedPay covers medical expenses for you, your passengers, or any family members involved in a car accident, no matter who’s at fault.

On the other hand, PIP goes a step further. It covers not only medical costs but also lost income and childcare expenses arising from the accident. It’s crucial to weigh the benefits of each coverage against their cost and decide which one suits your needs best.

One of the simplest strategies for saving on your car insurance involves adjusting your deductibles. A deductible is the sum you consent to pay out of pocket when filing a claim. Raising your deductible reduces the insurer’s risk, subsequently lowering your policy’s cost.

However, when choosing a deductible, it’s crucial to strike a balance. A $1,000 deductible is generally a good middle ground. It can help you save on premiums without being too much of a hit if you need to make a claim. It’s all about balancing your potential savings with your ability to cover the deductible in case of a claim.

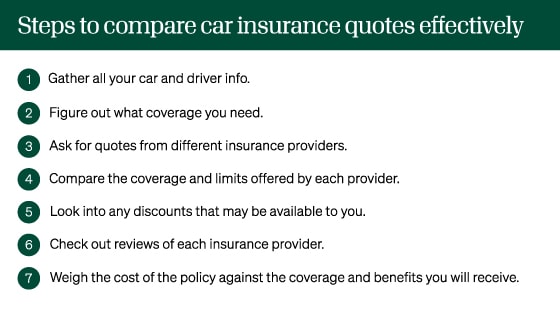

Shopping around for much car insurance can lead to significant savings. Comparing quotes from various companies guarantees that you secure the optimal coverage at the most affordable price.

But how do you compare quotes effectively? Here are the steps to follow:

By following this comprehensive approach, you will be able to make an informed decision and secure the best policy for you.

While full coverage car insurance seems like the pinnacle of vehicle protection, is it all necessary? Full coverage insurance combines numerous coverages to shield against an array of risks, including accident damages, theft, and other unforeseen incidents.

The cost of full coverage insurance can be influenced by various factors, including your age, where you live, and your driving record. It’s crucial to balance the cost with the protection it offers. If the yearly cost for full coverage is over 10% of your car’s actual cash value, you might want to consider dropping some elements of it.

In addition to the standard insurance coverages, there are also extra protections you can consider, such as gap insurance and other add-ons. Gap insurance covers the difference between what you still owe on your car loan and what your insurance company says your car is worth if it’s totaled.

There are also other add-ons like:

These benefits are useful features to have in your insurance coverage.

Car insurance requirements differ across states. Most states mandate a minimum insurance requirement, but the coverage amount can vary considerably. Notably, three states - California, New Hampshire, and Virginia - do not require car insurance.

In these states, drivers can prove their financial responsibility by showing they have enough money or assets to cover potential liabilities in case of an accident. Understanding these state-specific requirements is crucial to ensure you’re adequately covered and avoid penalties for driving without insurance.

Selecting the right deductible is a crucial part of your car insurance policy. Your deductible significantly influences your premium - a higher deductible results in a lower premium, and the opposite is true.

When choosing a deductible, consider factors such as:

If you’re comfortable with a higher risk for lower premiums, opt for a higher deductible.

Conversely, if you want less financial strain when making a claim, a lower deductible might be a better fit.

What factors affect your car insurance premium? Elements like your age, driving history, location, and your vehicle type can all determine your car insurance costs.

Factors that can influence your car insurance premiums include:

Now that we’ve covered all the ins and outs of car insurance, let’s talk about how to secure the right policy. This involves:

Remember, the cheapest policy may not always be the best. It’s important to balance cost savings with getting the right coverage for your needs. Additionally, don’t overlook the importance of good customer service. When you need to make a claim, you’ll want a company that handles claims efficiently and fairly.

In short, understanding car insurance can feel like navigating a maze, but with the right knowledge, you can confidently choose the coverage you need. Whether it’s deciding on liability coverage, comprehensive and collision insurance, or extra add-ons, remember to balance the cost with the level of protection you need. And don’t forget to shop around and compare quotes to ensure you’re getting the best deal. Remember, car insurance is not just a legal requirement, it’s a crucial financial safety net that protects you on the road.

Full coverage insurance includes liability coverage along with protection for damage to your own vehicle, while liability-only insurance only covers damages to other vehicles or injuries to other people when you're driving.

You would need collision coverage to cover the damage to your car from an accident, such as collisions with other vehicles or objects. Comprehensive coverage can also help repair damages caused by incidents like theft or non-collision-related damage.

Experts recommend aiming for at least $500,000 worth of bodily injury liability coverage to ensure comprehensive protection in case of an accident.

Collision insurance covers damages from accidents, while comprehensive insurance covers damages from non-collision incidents like theft, fire, or natural disasters. So, collision insurance is for accidents, and comprehensive insurance is for other incidents.